The Neocloud Transformation: A Comprehensive Strategic Evaluation of Nebius Group N.V. (NBIS)

The global technology landscape is currently navigating a structural transition from general-purpose cloud computing to specialized artificial intelligence infrastructure. This shift is characterized by the emergence of "neocloud" providers—entities built specifically for the high-density, low-latency requirements of large-scale AI training and inference. At the forefront of this movement is Nebius Group N.V. (NBIS), a company that has undergone a radical corporate metamorphosis to position itself as a full-stack AI infrastructure leader.

This report, prepared within the professional framework of Eastminds, provides an exhaustive analysis of Nebius Group, utilizing it as a primary case study for a standardized AI infrastructure evaluation template. The analysis integrates recent contractual developments, a deep dive into cash flow mechanics, and a rigorous technical assessment of price action through the lens of early 2026 market dynamics.

Strategic Corporate Evolution and the Neocloud Pivot

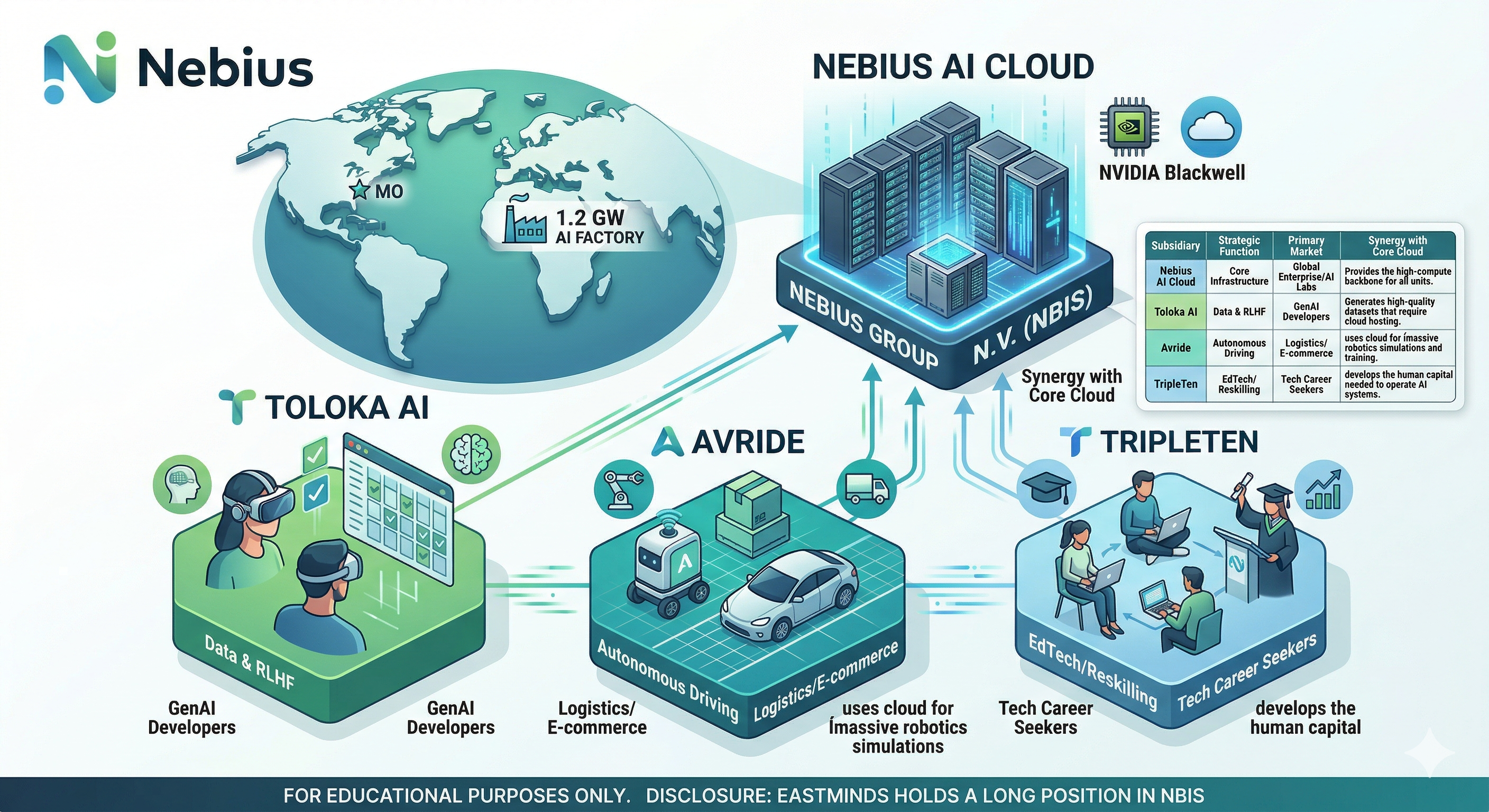

The narrative of Nebius Group is inseparable from its origins as Yandex N.V., formerly the dominant internet services provider in Russia. Following a complex and successful divestiture of its Russian-based assets in August 2024, the entity rebranded as Nebius Group N.V., effectively resetting its corporate identity to focus exclusively on the global AI market. This transformation allowed the company to emerge with a "clean" balance sheet, a deep bench of 1,300+ world-class engineers, and a headquarters in Amsterdam, Netherlands.

The underlying strategic trend suggested by this pivot is the decoupling of high-performance compute from legacy internet services. By shedding its diversified consumer assets, Nebius has eliminated the "conglomerate discount" and allowed investors to gain pure-play exposure to AI infrastructure. The company describes its core business, Nebius AI Cloud, as an AI-native platform designed from the ground up for demanding AI workloads. This involves a full-stack integration of proprietary software and hardware, a mechanism that distinguishes it from legacy hyperscalers like Amazon Web Services (AWS) or Microsoft Azure, which must maintain backward compatibility for millions of non-AI enterprise applications.

The company's geographic footprint is a deliberate response to the emerging "sovereign AI" movement. By operating R&D hubs in Europe, North America, and Israel, and deploying clusters across the US, UK, and the Middle East, Nebius provides regional data residency options that are increasingly required by national regulators. The implication here is that AI infrastructure is becoming a matter of national security and economic competitiveness, allowing specialized providers to capture market share from global giants who may face antitrust or regulatory friction in specific jurisdictions.

Subsidiary Ecosystem and Synergy Analysis

While the AI cloud is the primary revenue driver, the Nebius ecosystem includes high-growth units that serve as both customers and proof-of-concept laboratories for the core infrastructure.

The presence of Avride is particularly significant for long-term valuation. Avride develops autonomous cars and delivery robots for ride-hailing and e-commerce. The causal relationship between autonomous systems and cloud infrastructure is recursive: as physical AI becomes more complex, the demand for simulation-based training on GPU clusters increases exponentially. Nebius's collaboration with NVIDIA to build an end-to-end platform for robotics simulation confirms this strategic alignment.

Contractual Framework and the "Contract Machine" Phenomenon

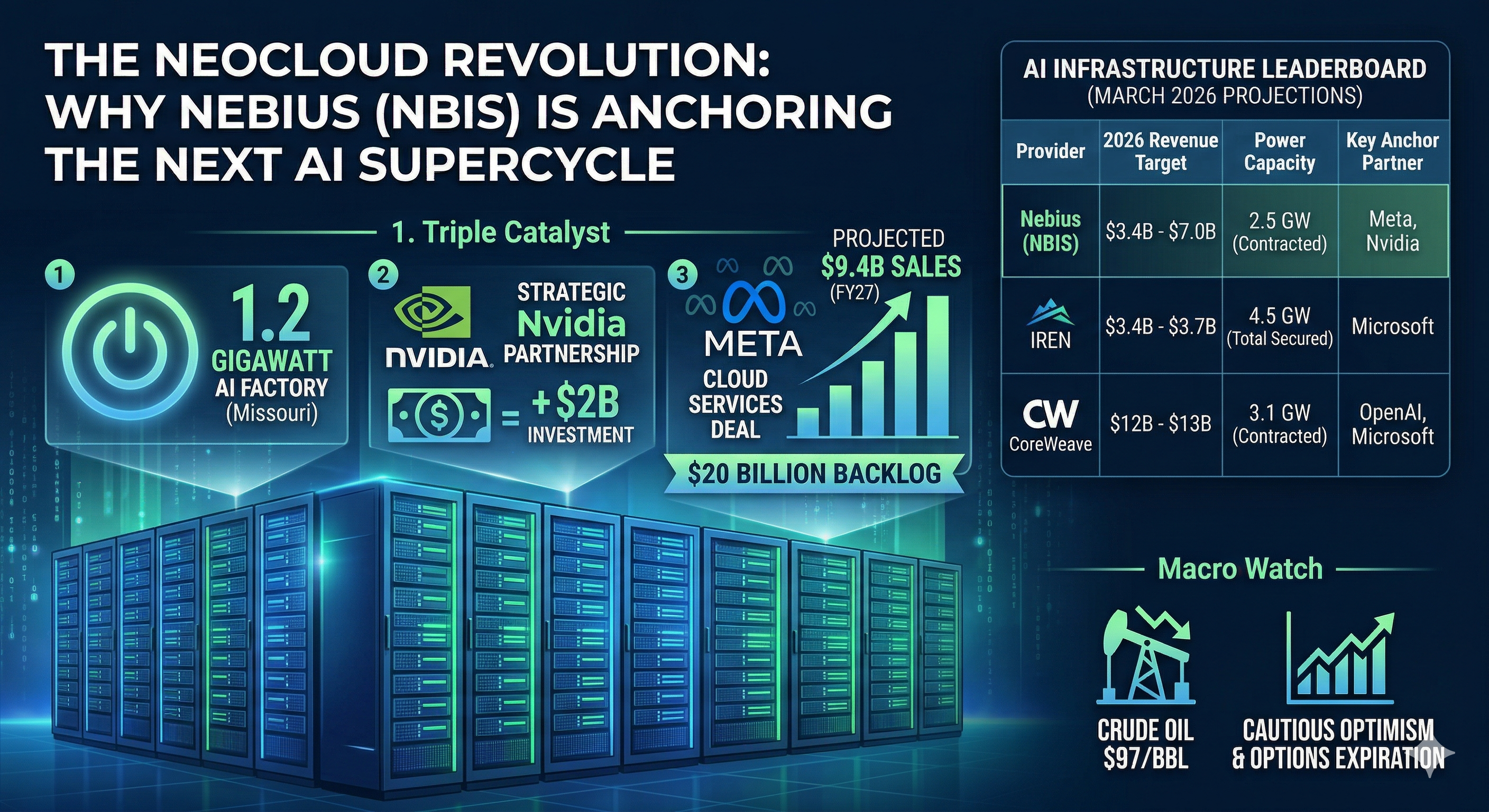

The valuation of an infrastructure-heavy company like Nebius is heavily predicated on revenue visibility provided by long-term service agreements. In early 2026, Nebius has demonstrated a remarkable ability to secure massive, multi-year contracts that de-risk its capital expenditure plans. This "contract machine" dynamic is a critical component of the Eastminds analysis template.

The Landmark Meta Platforms Agreement

In March 2026, Nebius announced a five-year AI infrastructure supply agreement with Meta Platforms, Inc., which serves as a definitive proof-of-concept for its neocloud model. This contract, valued at up to approximately $27 billion, represents one of the largest single commitments for specialized AI capacity in history.

The agreement is structured into two primary tiers:

Dedicated Capacity: Nebius will provide $12 billion of dedicated GPU-based capacity across multiple locations, with deployments beginning in early 2027. This capacity is based on the NVIDIA Vera Rubin platform, signaling that Nebius is a priority partner for next-generation silicon.

Flexible Commitments: Meta has committed to purchase up to an additional $15 billion of available compute capacity across upcoming Nebius clusters.

A deeper insight into this agreement is found in the "unsold capacity" clause. Under the terms, Meta is obligated to purchase any capacity in specified clusters that Nebius does not sell to third-party customers. This effectively provides a revenue "floor" for Nebius's upcoming expansion, allowing the company to aggressively build out data center capacity with a guaranteed buyer for its inventory. This mechanism reduces the risk of over-supply, a common fear in capital-intensive industries.

The Microsoft Revenue Agreement and NVIDIA Strategic Alliance

In addition to the Meta deal, Nebius has reportedly secured a multi-year, $17 billion revenue agreement with Microsoft, further cementing its position as a key supplier to the "Magnificent Seven". These agreements suggest a broader market theme: the hyperscalers themselves are facing such immense demand for AI compute that they are forced to outsource infrastructure to specialized players like Nebius and CoreWeave.

Supporting these contracts is a strategic partnership with NVIDIA. Nebius was validated as an "NVIDIA Exemplar Cloud," and in March 2026, NVIDIA disclosed a $2 billion strategic investment in the company. This investment is more than a financial injection; it ensures that Nebius has a "fast track" to hardware allocations during a period of global GPU shortages. This partnership also involves the deployment of 800 Gbps NVIDIA Quantum-X800 InfiniBand interconnects, making Nebius the first in Europe to run production GB300 NVL72 systems on this fabric.

Financial Performance and Capital Structure Analysis

The financial profile of Nebius Group reflects a classic "J-curve" growth trajectory. While the company is currently reporting significant GAAP losses, the underlying unit economics and top-line acceleration point toward eventual operating leverage.

Income Statement Dynamics

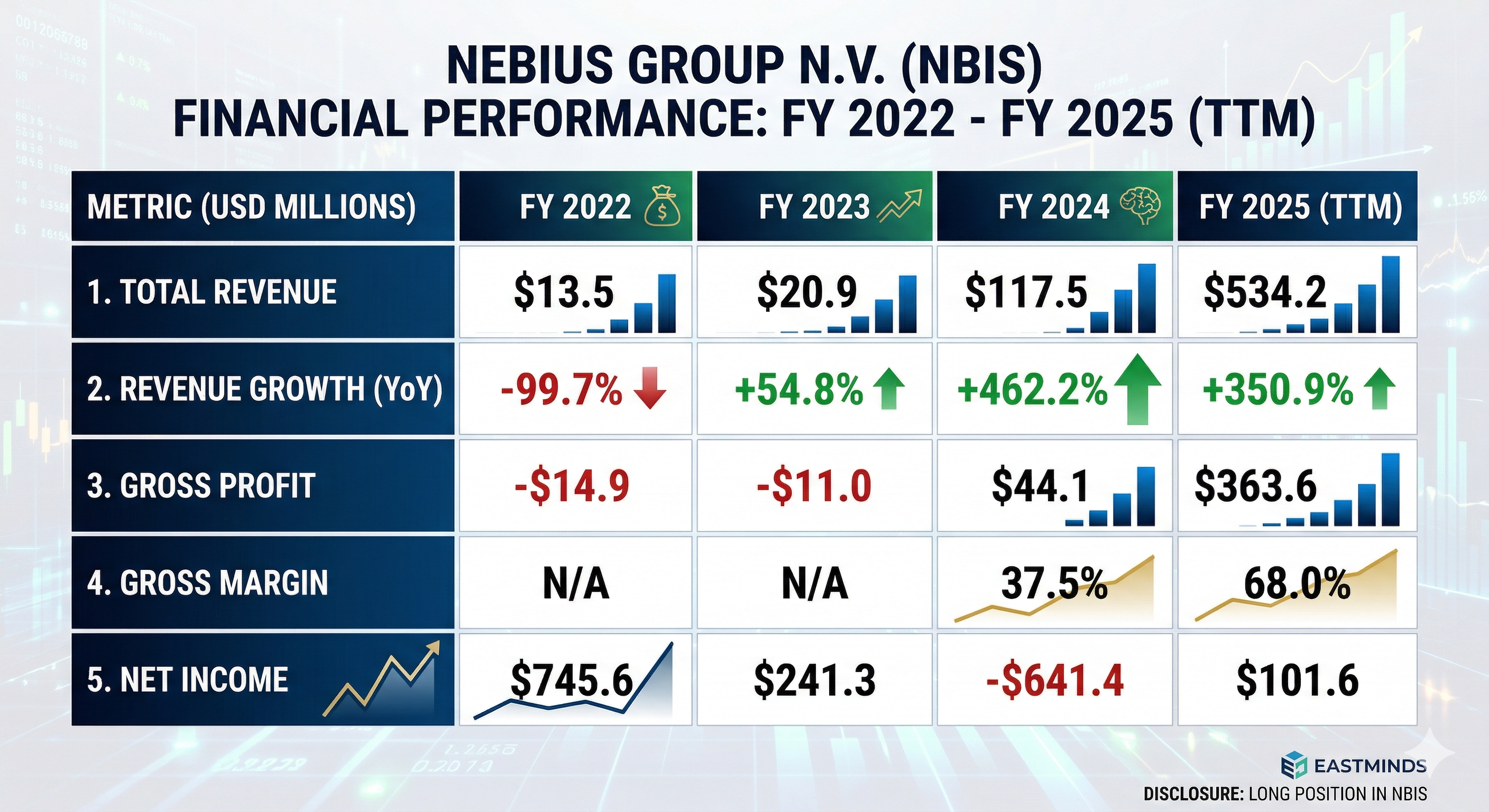

Revenue growth for Nebius has been explosive, driven by the rapid commissioning of new GPU clusters.

The massive revenue jump in 2024 and 2025 is the result of the company's full pivot to AI cloud services. The gross margin expansion to 68% in the trailing twelve months (TTM) is a critical data point, suggesting that specialized AI compute commands significantly higher margins than traditional cloud storage or SaaS applications. However, the net income figures are distorted by the divestiture of the Russian business in 2023/2024, which resulted in significant one-time gains and subsequent restructuring costs.

For 2026, the company has provided revenue guidance between $3.0 billion and $3.4 billion, a trajectory that would represent a roughly seven-fold increase from its current base. This guidance is supported by an Annual Recurring Revenue (ARR) target of $7 billion to $9 billion by the end of 2026.

Balance Sheet Stability and Debt Profile

As of the end of 2024, Nebius maintained a strong liquidity position with $2.4 billion in cash and equivalents against zero long-term debt. This was largely a byproduct of the asset sale to a consortium of Russian investors. However, the aggressive expansion required for the Meta and Microsoft deals has necessitates significant new capital.

In March 2026, Nebius announced the closing of a private offering of convertible senior notes, raising aggregate gross proceeds of approximately $4.3 billion. This capital raise is intended to fund the expansion of data center capacity from the current 220 MW toward a 1 GW target. While this infusion provides necessary liquidity, it also introduces dilution risks. The offering triggered a "buy the news, sell the dilution" reaction in the stock price, as investors weighed the benefits of expansion against the increased share count.

Cash Flow Analysis: The Engine of Infrastructure Expansion

For an infrastructure company, the cash flow statement is often more instructive than the income statement, as it reveals the true cost of growth.

Operating Cash Flow (OCF) and Earnings Quality

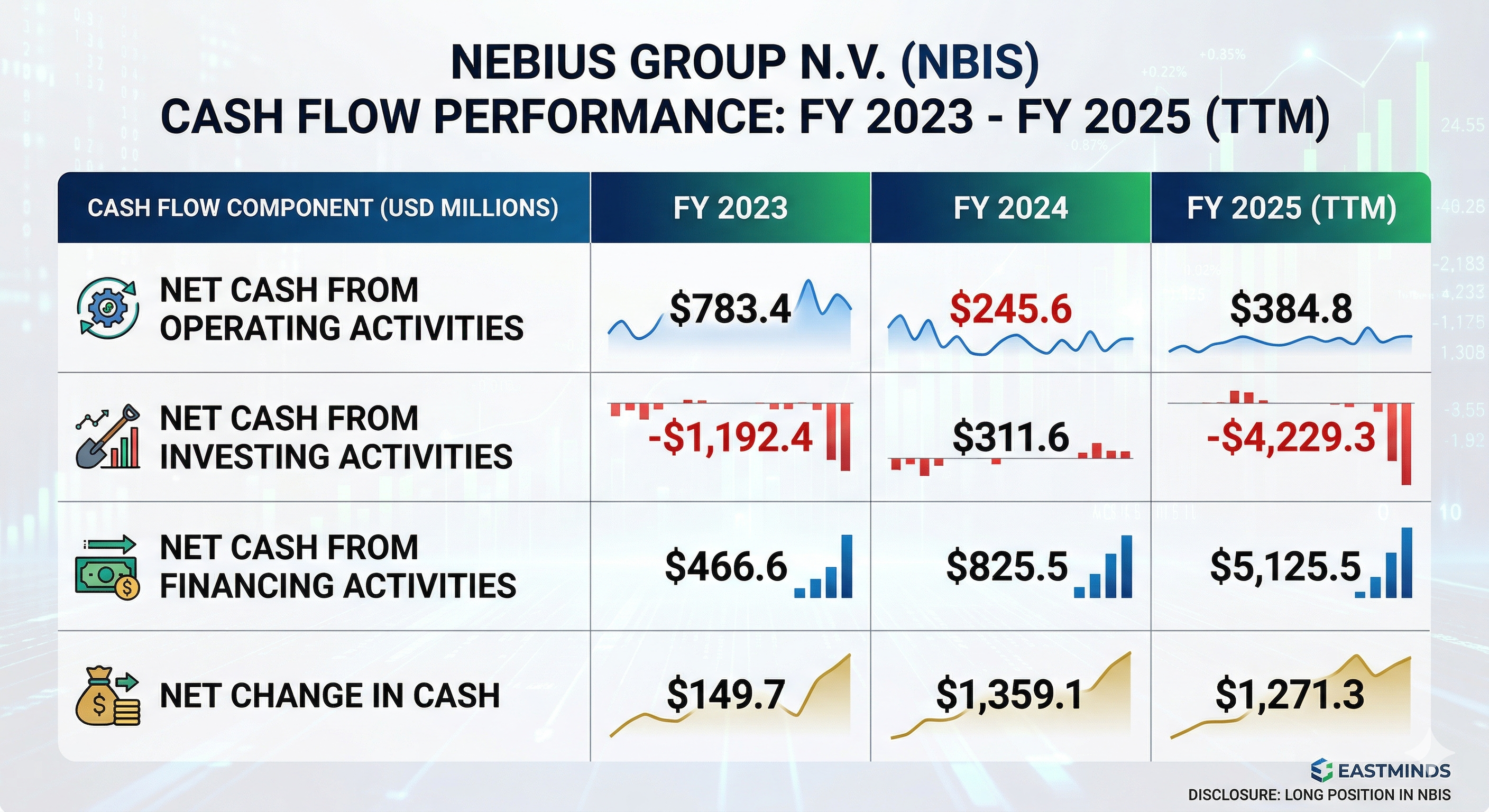

Nebius's earnings quality is currently described as "mixed." In 2024, the company generated $245.6 million in operating cash flow against a net loss of $641.4 million. This discrepancy is largely due to massive non-cash depreciation and amortization (D&A) charges ($421.5 million in 2025) associated with its hardware fleet.

The trend in investing cash flow is particularly revealing. In 2025, the company spent over $4 billion on property and equipment (CapEx), a four-fold increase from the previous year. This burn rate is the direct cost of acquiring NVIDIA Blackwell and Vera Rubin systems. The financing cash flow of $5.1 billion in 2025 reflects the company's reliance on external capital to fuel this growth.

Free Cash Flow (FCF) and the Funding Gap

Free cash flow remained deeply negative in 2024 and 2025. In FY 2024, FCF was -$562.1 million. By 2025, the funding gap widened as CapEx outpaced the growth in operating cash flow. This "negative FCF phase" is expected to persist through late 2026 as the company front-loads its infrastructure investments to meet the 2027 delivery dates for the Meta agreement.

The underlying causal relationship here is the "CapEx-to-Revenue" lag. There is typically a 12-to-18 month delay between the purchase of GPUs and the generation of recognized revenue from those chips. Therefore, Nebius's current cash burn is a leading indicator of its 2027-2028 revenue potential.

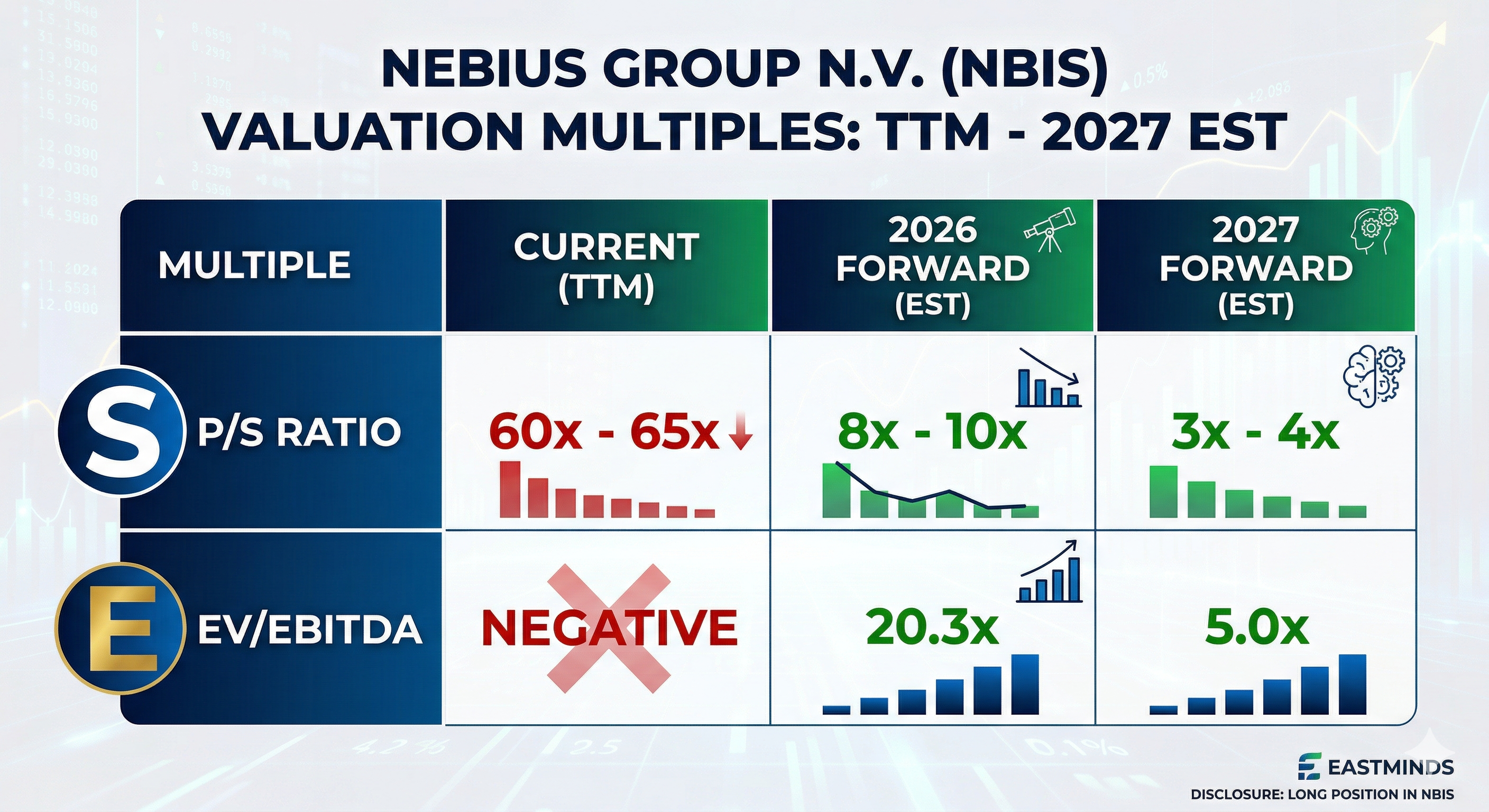

Price Projections and Valuation Modeling

Valuing a hyper-growth company like Nebius require looking beyond traditional P/E ratios, which are currently inflated (685x or 995x depending on the snapshot) due to the early stage of the revenue cycle.

Forward Multiples and the Rule of 40

A more accurate valuation model uses the Price-to-Sales (P/S) and Enterprise Value-to-EBITDA (EV/EBITDA) ratios on a forward-looking basis.

The massive compression in the P/S ratio—from 65x to 8x—over a single year highlights the sheer volume of revenue expected to come online in 2026. Analysts argue that if Nebius achieves its revenue targets and trades at a 20x forward sales multiple (a discount to its current 65x but in line with top-tier AI firms), its market cap could jump to $69 billion, implying a share price of approximately $276.

Analyst Target Consensus

Multiple analysts have issued updated price targets following the Meta deal and the NVIDIA investment.

- Median Target: $172.00

- Average Target: $182.75

- High Target: $243.60

- Low Target: $79.12

Recent ratings from Citigroup ($169), DA Davidson ($200), and BWS Financial ($200) underscore a broadly bullish sentiment that views the recent dilution as a necessary trade-off for long-term scale.

Risk Assessment and Market Constraints

The bull case for Nebius is robust, but the company faces significant operational and macroeconomic headwinds that could derail its projections.

Execution and Operational Bottlenecks

Nebius's growth is essentially a function of its data center capacity. The company has already leased out all available space as of late 2025. Any delays in the construction or commissioning of its new gigawatt-scale "AI factories" would directly impact its ability to fulfill the $20 billion+ backlog of sales orders. Furthermore, the company faced operational challenges in 2025, including an inability to meet surge demand, which led to a lowering of full-year revenue guidance to $525 million.

Supply Chain Dependency

Nebius is heavily dependent on NVIDIA. While the "Exemplar Cloud" status provides priority access, the company is still at the mercy of global silicon supply chains. If NVIDIA faces production issues with its Blackwell or Vera Rubin chips, Nebius would be unable to deploy its clusters on schedule, potentially triggering penalties or termination clauses in its agreements with Meta and Microsoft.

Financing and Dilution Risk

The funding of a multi-billion dollar build-out using convertible notes introduces permanent dilution. The $4.3 billion offering in March 2026 significantly increased the share count. If the company continues to rely on equity-linked financing rather than transition to asset-backed debt or corporate cash flows, the "per-share" value of the growth may be severely muted for current investors.

Conclusions and Investment Thesis

The strategic evaluation of Nebius Group N.V. reveals a company that has successfully positioned itself at the epicenter of the global AI infrastructure build-out. By pivoting from a Russian internet giant to an Amsterdam-based AI neocloud, the company has secured the engineering talent and geopolitical neutrality required to serve as a primary infrastructure partner for US hyperscalers.

The landmark $27 billion agreement with Meta Platforms serves as the ultimate proof-of-concept for the Nebius business model. The "unsold capacity" commitment from Meta materially de-risks the company's $4 billion+ annual CapEx program, providing a level of revenue visibility that few other mid-cap technology firms can match. While short-term technical indicators suggest a period of consolidation and the $4.3 billion convertible note offering introduces dilution concerns, the long-term fundamentals remain exceptionally strong.

The Eastminds analysis indicates that if Nebius can successfully navigate the operational challenges of scaling its capacity from 220 MW to 1 GW, the stock is well-positioned to reach the median analyst target of $172.00. The transition from negative free cash flow to positive adjusted EBITDA in 2026 will be the key catalyst for the next leg of the rally. Investors should view NBIS not merely as a cloud provider, but as a "physical AI" play whose infrastructure is the essential substrate for the next generation of autonomous systems, LLMs, and enterprise AI agents.

The core of the investment thesis is the "CapEx-to-Revenue" conversion. With a confirmed backlog exceeding $20 billion and strategic backing from NVIDIA, Nebius is no longer a speculative play but a fundamental infrastructure provider for the AI era. For professional peers, the monitoring of quarterly GPU deployment schedules and data center power-up dates will be the most critical metrics for assessing the company's progress toward its ambitious 2026-2027 revenue targets.

Disclosure & Market Disclaimer

Position Disclosure: At the time of publication, Eastminds (or its managed accounts/affiliated entities) holds a long position in Nebius Group N.V. (NBIS). We may buy or sell shares at any time based on market conditions and our evolving investment thesis without further notice.

General Disclaimer: This article is provided for informational and educational purposes only. It does not constitute financial, investment, tax, or legal advice. The "Neocloud" and AI infrastructure sectors are subject to high volatility, significant capital expenditure risks, and rapid technological obsolescence.

Risk Warning: Investing in individual equities involves a high degree of risk, including the potential loss of principal. Past performance—including the technical setups and historical rallies discussed herein—is not indicative of future results. Always perform your own due diligence and consult with a licensed financial advisor before making any investment decisions.

Get Weekly Market Signals

Join the mailing list for top aggregated insights. No spam, ever.